Debt Without End

Why global public debt stopped being countercyclical and became permanent

Dear readers, good morning.

I haven’t acknowledged all the new subscribers in a while, so a warm welcome to you and thank you for being here!

Switzerland, where I am based, is getting sunnier, and life in the city feels so different when it’s warmer. People are more smiley, streets are busier, and I am starting to understand why it is ranked at the top in quality-of-life metrics. Believe me, it took me some time, because for 8 months of the year all I see is grumpy people in the tram and grey skies. So while I was cycling in the city center on Wednesday, looking at the Opera House plaza in Zurich and the mountains in front of me, I realized I had no idea how Switzerland finances all of this. How does a country with so much infrastructure and generous public services end up with so little debt? And why is that the opposite of other places I know?

We, younger generations, do not seem to care much about public debt. But that metric determines whether we’ll pay more taxes, have a decent pension, and how public services will evolve as we grow older. Most of us worry first about closing the credit card at the end of the month. But governments do not seem to care as much about their own balance sheets. Except for a few. Like the Swiss.

The old paradigm is dead

For most of modern history, the rule was simple. Governments borrowed in wartime and paid down debt in peacetime. That rule is no longer operating.

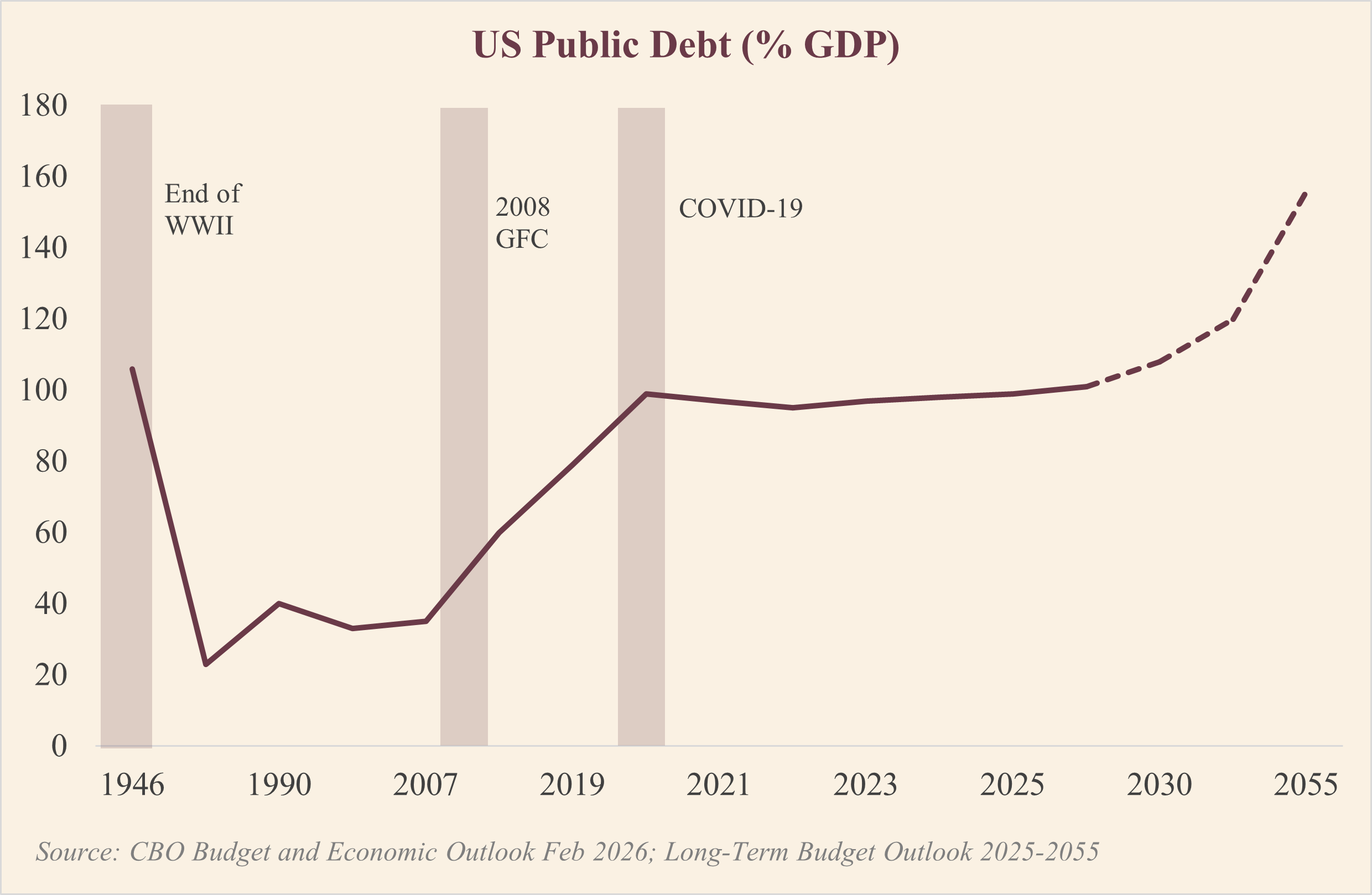

Global public debt is now approaching 100% of GDP, heading to levels last seen just after World War II1. The difference is that nobody is at peace long enough to pay anything back. Every crisis of the past twenty years has added a layer, and none has been unwound. 2008 put private losses on sovereign balance sheets. COVID piled on. Then Russia-Ukraine. Now the US-Iran war and a global rearmament cycle.

Sovereign balance sheets are now the stress point of the system, precisely when interest rates are structurally higher than they were for the entire post-2008 decade. If discipline comes from anywhere now, it is from the bond market, not from fiscal policy. What that means in practice is simple: when investors start doubting a government’s ability to pay, they demand higher yields to hold its debt. Borrowing costs rise, interest payments eat more of the budget, and eventually governments are forced to adjust spending whether they want to or not. The market does the job that politicians will not.

The US: growing deficits and debt

US debt held by the public is projected to reach 120% of GDP within a decade. The annual deficit is running above 5% of GDP in a non-recession year2. Wartime numbers, printed in peacetime.

What matters more than the number is the trajectory. Interest payments are now the second largest item in the US federal budget. And the average interest rate on the national debt is projected to overtake the growth rate by the early 2030s. Once that happens, you cannot stabilize debt through growth. The options left are: cutting spending, raising taxes, or inflating the debt away. The American youth pays no matter which one is chosen.

The global rearmament

I wrote about this last year, and the structure has only sharpened.

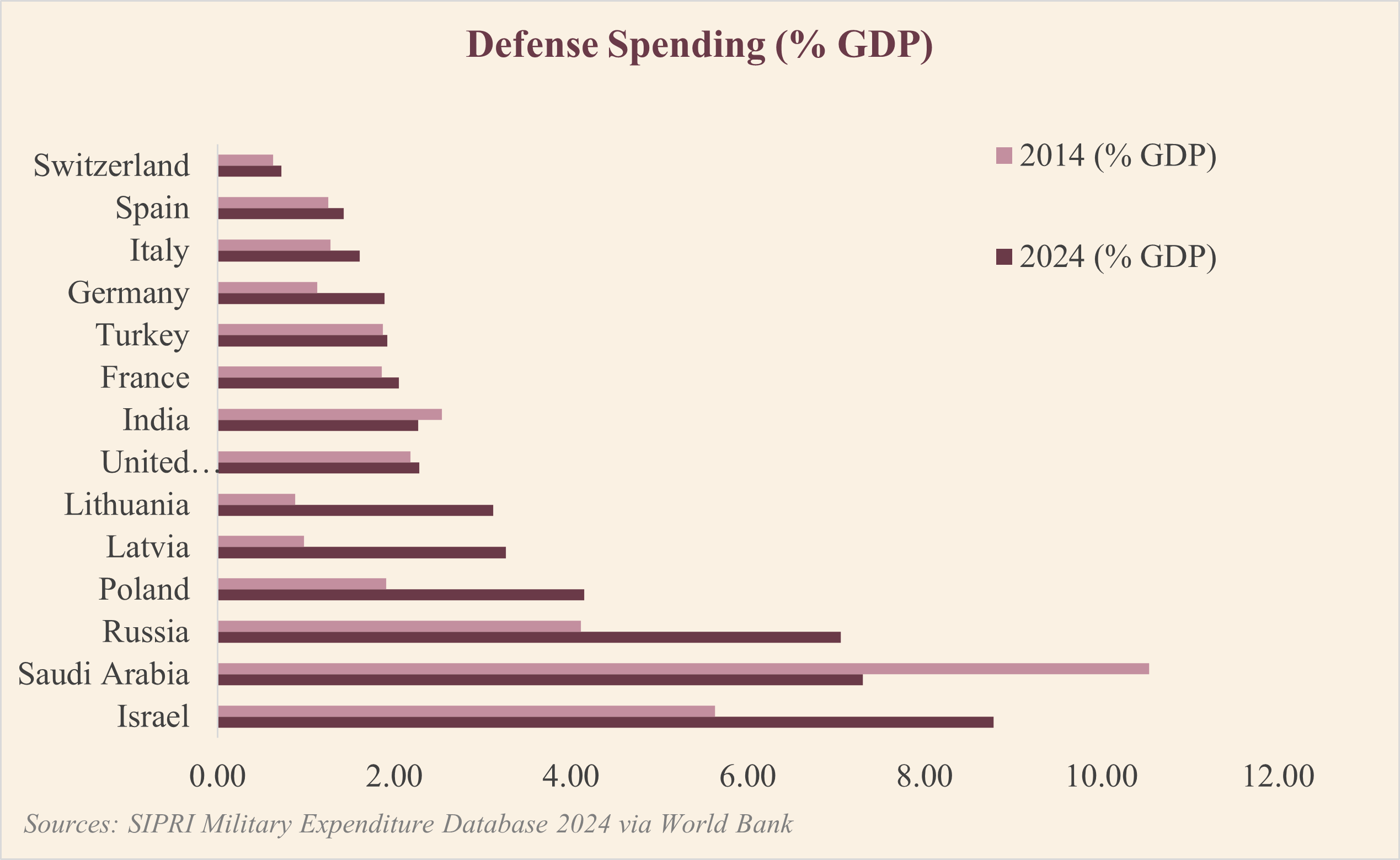

Half the world’s countries increased defense budgets over the past five years. NATO committed to 5% of GDP by 2035, more than double the old benchmark. The IMF has studied every major military buildup since 1946, and the pattern is always the same. Governments promise to pay for it later. Later turns out to mean borrowing. Within three years, the debt pile is meaningfully bigger. In wartime, twice as bad3.

Europe has a second layer of the problem. It does not produce most of its own military equipment. Around 80% is imported, mostly from the US4. So European taxpayers are borrowing money to send to American defense companies. And this is no longer a Western story. China is expanding, India is scaling up domestic arms production, and Turkey has become a drone exporter. Military investment is what the next decade of deficits will be spent on.

So Europe is committing to decades of higher deficits to fund defense at a time when it is also trying to finance pensions for an aging population, a green transition, and healthcare. These demands compete in the same budget. When defense wins, something else gets squeezed.

The price of every shock

The US-Iran war is the most recent layer on the stack with higher oil and gas prices. And now even countries sitting on large oil reserves are quietly scaling back their projects because the fiscal math no longer works at current spending levels.

The pattern across 2008, COVID, Russia-Ukraine, and now Iran is the same. A shock lands: governments respond, because not responding is politically impossible. Debt rises. A promise is made to normalize later. Later never arrives, because the next shock is already on the way.

Every shock absorbed on the sovereign balance sheet today is a future cut to a public service, a tax hike, or a piece of infrastructure that does not get built.

This is what people mean when they say the 2020s will be remembered as the decade when public debt became structural.

Switzerland: another game

Back to the view from the Opera House plaza.

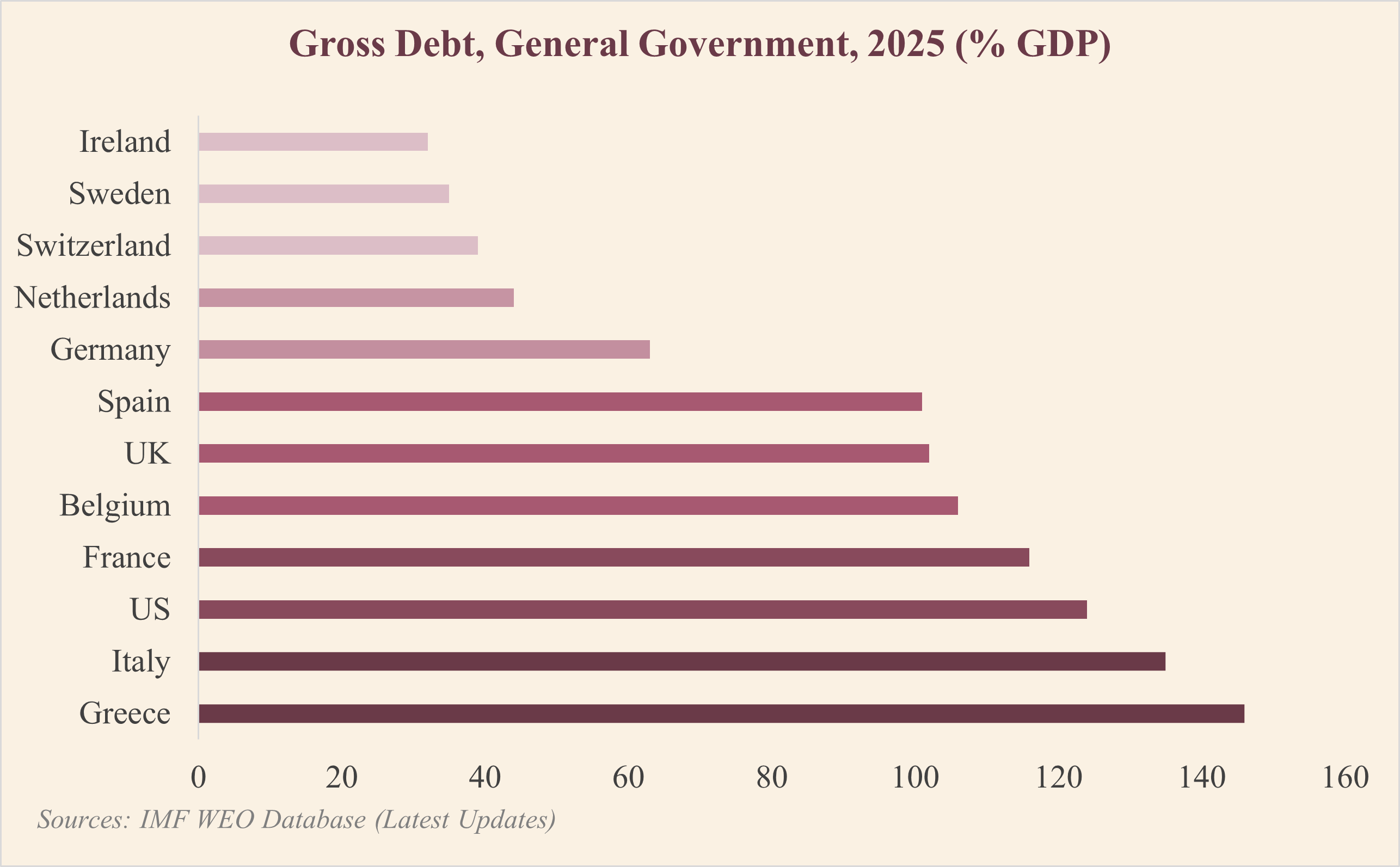

Switzerland’s gross public debt is around 38% of GDP. The country ended 2025 with a small financing surplus, and yet the Federal Council is already flagging potential deficits from 2027 onward.

The reason is something called the debt brake, implemented since 20035. Think of it like a household budget rule. In a good month, when you earn more, you save. In a bad month, you can spend the savings, but you cannot keep borrowing indefinitely. The Swiss applied that to their government. In good years, surpluses are required. In bad years, deficits are allowed, but only up to the size of past surpluses. Exceptional events like the pandemic go on a separate tab that has to be paid off on a fixed schedule.

Germany copied the model in 2011, and most of the EU adopted a version the following year. Germany has since had to amend its own rule to allow more borrowing for defense, which tells you how binding these frameworks really are once geopolitics gets in the way.

The contrast is striking. Switzerland has the best infrastructure, great public services, and a debt ratio a fraction of its peers. Meanwhile the US is past 120% of GDP, the euro area is set to break 90% on current trajectory, France is above 110%, Italy above 135%6.

Every major developed economy faced the same shocks over the past two decades. One set of them absorbed the hits and kept borrowing. The other had a rule and is still the most livable country in the world.

(Although I’d still contest that a bit. I think that the most livable places in the world are those that are sunny all year long and have good music. But let’s be honest, no plausible income is generated in these places.)

A note on debt measures: This piece uses CBO's "debt held by the public" for the US (around 100% today), which captures what the federal government owes to outside investors. For international comparisons it uses the IMF's general government gross debt (US currently 123%), which is broader and includes state and local government debt plus intragovernmental holdings. Both measures tell the same directional story.

IMF Fiscal Monitor, October 2025

Congressional Budget Office, February 2026.

IMF, World Economic Outlook, April 2026

Mario Draghi, The Future of European Competitiveness, September 2024.

Swiss Federal Department of Finance, "The Debt Brake at a Glance"; Swiss Constitution, Article 126

IMF WEO Database